“100% Guarantee For Your Rental Home!” Delightful or Sour?

Tommy: Here’s how I see it. A guy puts a guarantee on the box ’cause he wants you to feel all warm and toasty inside.

Ted: Yeah, makes a man feel good.

Tommy: ‘Course it does. Ya think if you leave that box under your pillow at night, the Guarantee Fairy might come by and leave a quarter.

Ted: What’s your point?

Tommy Boy (1995)

My 9-year old son was eating frozen blueberries a few weeks ago and started to complain about them. “They’re so sour! Gross!”

I advised him, “Well, that’s too bad. You get some good ones, and you get some bad ones. It’s the way life goes…” Then I patted myself on the back for imparting some timeless, Forest Gump parenting advice.

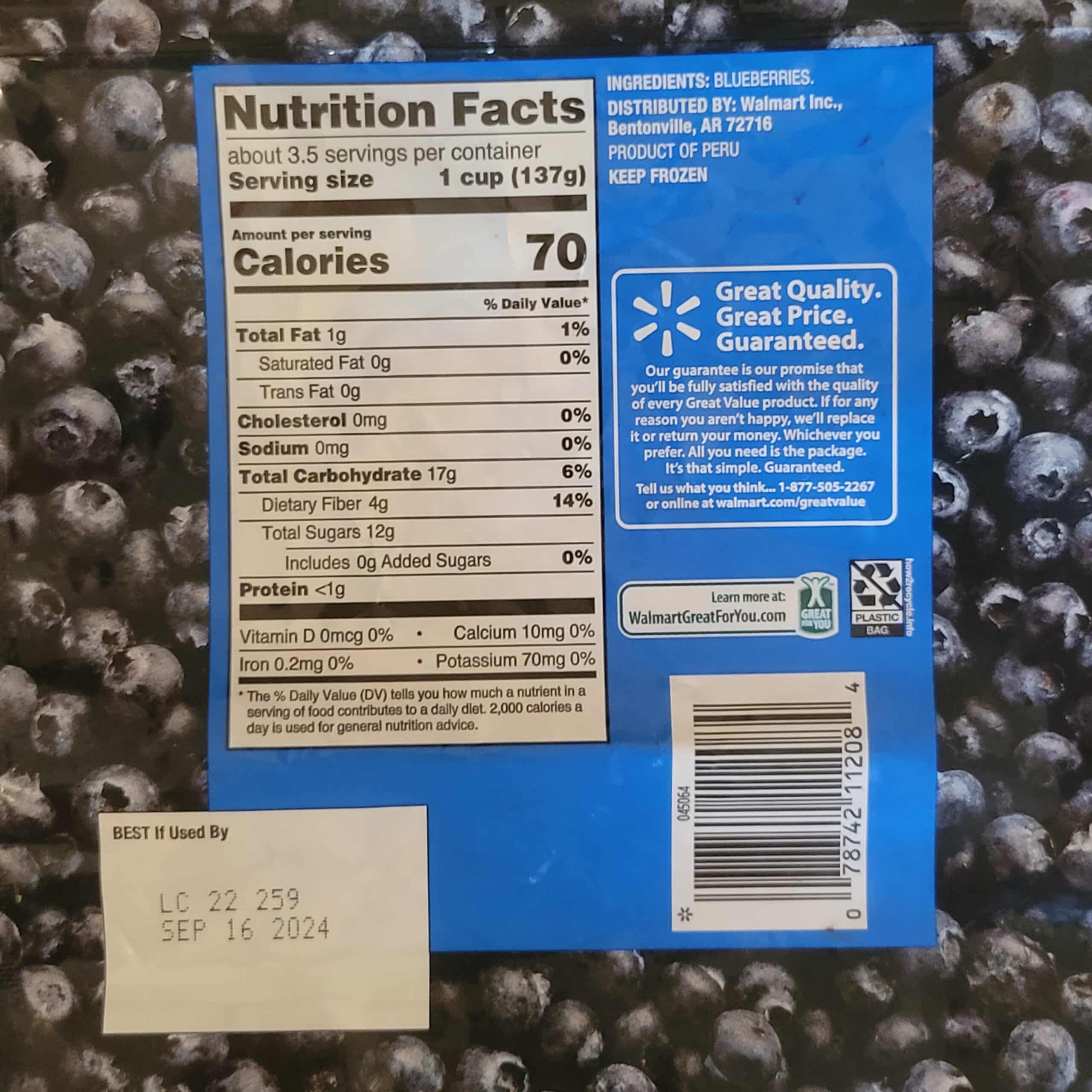

Sometime later, he complained again- and then three or four other times after eating these blueberries. Finally, I grabbed the package off the table and saw it was the “Great Value” Wal-Mart brand. My eyes narrowed on the “Great Quality. Great Price. Guaranteed.” guarantee printed on the back. Verbatim, it read:

If for any reason you aren’t happy, we’ll replace it or return your money. Whichever you prefer. All of you need is the package. It’s that simple. Guaranteed.

Now was the time to teach my son about the advantage of paying attention and reading the fine print! “Son, we’re going to Wal-Mart and you’re going to take care of it.” “Dad, are you sure we can bring this package in and they’ll give us the money back? I’ve already eaten half of them…” “Yes, son. It’s that simple. Guaranteed!”

After my son negotiated that he could keep the $2.99 windfall and put it towards a pack of football cards, he signed on to this gambit. We drove over to Wal-Mart and, from a distance, I watched my son explain to the customer service person that the blueberries were sour and that he wanted a refund. After a minute or so, he walked away from the counter, defeated, and let me know that we could swap it out for another bag of (sour) blueberries; there was no option of getting football card money instead.

Now Dad was sure there was a misunderstanding! It’s guaranteed! It’s simple! And it’s a $2.99 charge to a multi-billion dollar conglomerate! Well, yours truly fared no better when I approached the customer service desk and was promptly (but nicely) shut down. If I didn’t have the receipt or credit card it was bought with, their hands were tied. There was nothing that could be done.

Undeterred, as my young kids trolled the Wal-Mart aisles unattended, I called the #800 number that was located under the guarantee. After a 14-minute phone call of providing serial numbers, date of purchase, and personal information, the customer service representative (who was also very nice) said that we would receive a $5.00 Wal-Mart gift card mailed to us within 2 weeks, but no cash. When we got home, I sent a message through the “Great Value Guarantee” website and they referred me to the in-store customer service desk for any refund requests. I wrote back saying that was where it all started! Then I never heard back. Ugh!

If for any reason you aren’t happy, we’ll replace it or return your money. Whichever you prefer. All of you need is the package. It’s that simple. Guaranteed.

The final scorecard read: (1) in-store visit, (1) 14-minute phone call, (1) web inquiry, & (1) 2-week wait for a $5.00 store credit. So, obviously, it’s not that simple. And it’s far from guaranteed. And we are talking about getting $2.99 back from Wal-Mart which they explicitly stated was a sure thing on the package itself.

Great story! But what’s your point? What does getting a cash refund for a sour bag of Great Value frozen blueberries have to do with property management?

A lot, actually. It’s about the danger of relying on corporate guarantees when picking vendors, especially in real estate. Whether it is for home warranty insurance against bigger ticket items breaking down (HVAC systems, roofing, appliances, etc.), costly property management occurrences (eviction, pet issues, etc.), or just getting money back from poor work (a flooring vendor recently), it is difficult to get companies to honor them. No company wants to pay (not even $2.99!) and there is always a reason why the guarantee doesn’t apply. It’s frustrating, (super) time-consuming, and borderline unethical at times.

But that doesn’t stop them from being ubiquitous:

- Home warranty companies: “If your HVAC system goes down and it can’t be fixed, we’ll buy you a new one! It’s so simple. Guaranteed!”

- Property management companies: “If there is an eviction or pet damage, we’ll cover the costs- It’s so simple! Guaranteed!”

- Wal-Mart: “If for any reason you aren’t happy, we’ll replace it or return your money. Whichever you prefer. All of you need is the package. It’s that simple. Guaranteed.”

Life is too short. The best bet is to pick a company that consistently offers quality blueberries instead of trying to be compensated on the backend when they are sour. Getting the $2.99 back is arduous at best, and unfortunately, usually fruitless. Be wary of upfront guarantees and concentrate more on established track records of excellence!

Happy Landlording!

Learn More

Finding Value & Buying Rental Homes on Your Credit Card

Fresh out of college, I was living in New York City and was slinging cell phones by day (they were relatively new back then) and dreaming big dreams at night. How could I become financially successful like many of the people I was passing on Wall Street everyday? I wasn’t overly into finance, but started reading a lot of material from the real estate gurus. Be a millionaire with no money down! Live off of passive income to live the life you’ve always imagined! It’s so easy anyone can do it!

That sounded right up my alley- easy and something even I could do. If that mother of 6 in El Paso could be netting $25K month in passive rental income, surely I could do half of that? I was all-in. Unfortunately, New York City real estate was prohibitively expensive for me to buy (got $1M to plunk down?), so I wasn’t sure how I would get started.

So I moved to Charlotte and became a full-time Charlotte real estate investor. The $1M homes were replaced with much more affordable options. I posted classified ads (“We Buy Homes!”) and tried to follow the guidelines from the infomercials. I joined an investment club and started getting calls and e-mails for discounted homes to buy.

Many of the homes were really cheap, some to the tune of $50K. The problem was to what to do with them after purchase. Most people didn’t want to live in them as they were in “war zones”. I’ve never been a gun guy, but visiting some of these homes made me think hard about my self-protection stance. I didn’t feel overly safe at many of them and replacing broken windows constantly didn’t seem economically savvy. So I, and others, passed on buying many of these homes (laughable now, right?) and they languished on the market for months and years.

One day, I visited one of these types of homes and was not really interested. The seller said she was negotiable on price, but I liked being alive and really didn’t want to be involved. Plus, she said she needed to close really quickly and needed cash, and I didn’t have a ton of cash on hand. I figured I’d ask what she was looking for before declining.

$8K.

Well $8K was in my wheelhouse. I wrote up the contract and asked the closing attorney if he would take one of my Visa checks that came in the mail earlier that week from my credit card company. No problem!

Did I want this house? Not really. It came with issues. I had to sink another $20K into it just to make it habitable for a rental. And the area wasn’t great. But $8K? Come on! I had to do it.

I learned that every asset had a price.

I got a call recently from a prospective client who asked me if her home had a realistic chance of renting. It was in a desirable area and she lived there currently, but the kitchen wasn’t redone and it had an older layout. Did she need to sink $50K-$100K into it before it could go to market?

The answer, without even looking at it, was “yes” and “no”. The real question was how much she wanted to rent it out for. Would it rent for as much as the remodeled home down the street if it wasn’t renovated? Probably not. But depending on the rental price, someone would gladly take it. There are 66 people on average moving to Charlotte every day who need a place to live!

Real estate, like anything, is a value proposition that has a suitable price. A rental house priced at $3K/month may sit, but at $2K it may fly off the market. Value is what matters. Top conditioned homes will rent out the highest, while homes in poorer condition will rent out for less. The market is relatively efficient.

Happy Landlording!

Learn More

Where to Invest in Real Estate in Charlotte?

As a property manager in Charlotte with investor clients, we are often asked where the best places are to buy local investment properties.

When I was a young real estate investor in 2004, I bought my first two investment properties on the same day from HUD. Both were relatively cheap and I figured they’d be easy to cash flow. I admittedly did not really know what I was doing.

One was a condo in a relatively contained area. The other was a house in what could be labeled a “war zone”.

I hated this house. If I was smarter, I would have outsourced the property management. One of the main issues is that it would just get broken into a lot. So every time it was vacant, I was praying that I didn’t have to have the windows and doors repaired again. The house was really old and somehow the utility bills were really high, which added to the vacancy pain.

One day I was stopping by the house and noticed a man with a shopping cart full of old window screens walking in the neighborhood. I didn’t give it much thought (like I said, it wasn’t a great area) until I reached the house and noticed something a little off about the (formerly) screened-in porch. I ran back to my car to find the guy with my screens.

He was still on the street. I pulled up behind him in my car and he kept walking. I got out and walked quickly to catch up to him.

“Excuse me, sir? I think you may have something that belongs to me.”

No response. He kept walking away at his measured pace.

“Yeah, I’m sure of it- those seem to be the window screens from my house up the block. Mind if I take those back?”

He stopped, turned around, grunted, and then lunged at me with a knife. Fortunately, he missed due to my cat-like reflexes (OK, not true) and the fact that he was drunk and slow (thank God!). He then kept walking away.

I followed him in my car and called the police. He smartly cut across a field and was never seen again.

As I left the scene with my tail between my legs, there was nothing left to do but go back to the house and re-shoot the front porch pictures. Then I logged into my computer and changed the rental ad copy from “Awesome House with Screened-In Porch!” to “Awesome House with Open-Air Porch!”.

Oh, how I hate(d) that house!

Fast forward approximately 13 years… the Charlotte press started fawning over this “new” area of Charlotte that was having all of this awesome new development. Price values were skyrocketing; it was the next big thing. As I clicked through to read further, the area they were referring to was very familiar… No way… The smart money wanted to be in the vicinity of “that house”.

A popular calculation is that 66 people are moving to Charlotte every day. The Charlotte-Metro population is set to go up 50% in the next ten years. And all of these newcomers need a place to live.

As a real estate investor, the short-term prognosis on where to buy in Charlotte is a crapshoot; an efficient market should have already built this into the current prices. However, due to population forecasts, the long-term prognosis of where to invest is much surer. “That house” (or any house in the city of Charlotte) will probably be a good investment you’ll love if it’s held long enough.

Happy Landlording!

Learn More

Too Big of a Jump to NBA Competition (& Rent)?

What do former NBA players Jack Sikma, Devean George, Vern Mikkelsen, and Terry Porter have in common?

I’m a big basketball fan, but had only heard of 3 out of the 4. And I had no idea what they had in common.

Answer: They all came to the NBA after playing at a Division 3 college. That’s pretty hard to do. It’s so hard, in fact, that they are the ONLY players to ever make it to the NBA from Division 3 schools.

Why is that? The best high school basketball players have either gone directly into the NBA (ex: LeBron James) or gone via a Division 1 college (ex: Kemba Walker from the University of Connecticut). The competition in Division 1 is fierce and players train year-round to compete. And 99%+ of Division 1 players are not good enough to play in the NBA.

Division 3? Though the players are very good if they are playing hoops in the park with you, most would probably have a hard time competing against a Division 1 player’s athleticism, size, and skill. Those Division 1 guys are really good! And multiply that by 100 for the guys who are good enough to play in the NBA.

So am I a Division 3 hater? Not at all! I can probably relate to them much more on the basketball court. But when they have to try to play against NBA-caliber players, it’s just too much of a jump. The NBA guys are stronger, faster, quicker, more accurate, have better basketball IQ, and jump a lot higher. Most Division 3 players don’t stand a chance. It’s like trying to compete against a perfect storm of genetics and work ethic.

I sometimes feel like I run into this situation with rental applications.

BDF Realty receives some applications from perfectly fine, average tenants. They have decent credit scores, a few late payments from their prior landlord, and have some debt. But we have to turn them down. Why?

Because they were only paying $900.00 in rent and want to rent a house that rents for $1,500.00. With rising rents in Charlotte, this has become a more common situation.

We have to ask: if the tenant was late a few times at $900/month and apparently has consumer credit card debt that is being carried from month-to-month (aka living beyond their means), what is it going to look like when the rent jumps up to $1,500/month? Where is that extra $600/month coming from? It would require a lifestyle change that most people don’t want to and/or are unable to make.

It’s certainly not impossible. But just like the aforementioned four Division 3 players being the only players to make the NBA, it is unlikely to work out. The jump in rent is usually too great.

No one (tenant or landlord) wants a situation where it is a struggle to make ends meet. Be cautious when accepting tenants who might not be equipped to make the big jump into the NBA.

Happy Landlording!

Learn MoreCharlotte Property Management Weekly: “List to Last” Still True?

There are many sayings that become axioms as their wisdom becomes evident over time:

“Don’t throw good money after bad”

“The way to a man’s heart is through his stomach”

“Diamonds are a girl’s best friend”

In real estate, the wisdom for real estate agents was “list to last”; this means that the agents who want to last in the business should take a lot of sales listings (aka put houses on the market for sale). The rationale is that if an agent has a lot of houses on the market for sale or rent, it is probable that some of them will and they’ll make money.

Taking listings requires resources from agents. Agents need to take pictures, gather information, put the listing up on websites, take phone calls, and then pay for advertising. There is also the time expended fielding inquiries about the home, showing it to potential buyers, and giving status reports and tips to their seller clients. The more homes the agent has on the market for sale or rent, the more resources that are required.

And this isn’t a paid gig! The agents are working on faith that some of the houses will sell and they will be reimbursed for their expenses. Agents are putting themselves into position to be lucky. Fortunately, in the past, this usually worked out well.

Now, however, houses aren’t selling very swiftly. And more people than ever want to sell their homes. “List to Last” can be the fastest way to go broke. Agents that were salivating over the amount of listings they were personally accumulating are now singing a very different tune. Not only are they being sucked dry financially, the toll of anxious seller’s phone calls are sucking them dry psychologically.

“Why isn’t my home sold yet? You said you were different!”

“Why haven’t there been more showings? Why aren’t I seeing any offers?”

“Are you any good? How much money are you spending to advertise my property? You are just one of those agents who puts the home on MLS and then sits back to collect the commission, aren’t you?”

“List to (Not) Last” or “List to Leave (the Business)” may seem more apropos axioms. Amassing home listings that don’t move is both financially and mentally taxing. So what to do?

One word- Prequalify. In a world of limited resources, agents need to expend their resources judiciously. They need to know with a high degree of certainty that they can execute a transaction for a client. This is already commonly done by buyer agents who won’t show properties to clients who aren’t prequalified by a bank to purchase. This needs to be the norm on the sell side as well. That means not accepting every listing opportunity (gasp)!

Specialized firms do this everyday. Auction firms take listings that they know they can sell; if the client isn’t willing to (or can’t) take whatever offer that comes, they don’t expend their resources to put it on the block. It’s the same with short sale firms. If a client isn’t willing to let their credit get shredded, they typically won’t walk through the firm’s doors. Clients prequalify themselves.

General brokerage has a “come one, come all” message; prequalification of clients is done at the individual agent level. And, to have staying power in the real estate business, it’s important that it actually happens!

Listings are still vital to the business of real estate agents, but they need to be homes the agents know they can sell or rent. So, in the new normal, the axiom should read, “List (the Homes You Can Actually Transact) to Last!”

Brett Furniss is the President & Owner of BDF Realty (“Charlotte’s Most Innovative Property Management & Investment Company”), and Rent-To-Sell Realty (“When You Need a New Solution to Sell Your Home”) which specialize in rent-to-own (lease options) and rent-to-sell homes. His newest book, A Real Estate Agent’s Complete Guide to Representing Rent-To-Own (Lease Option) Tenants (Delight Clients, Fill Vacant Homes, and Earn $2,250* Upfront! (*Minimum!)

Learn MoreCharlotte Property Management Weekly: Why Rent-To-Sell is “Hot, Hot, Hot” in Today’s Cold Real Estate Market

Q: Why do robbers rob banks?

A: Because that’s where the money is

Q: Why have home sellers shifted their vacant homes from “for sale” to “rent-to-sell”?

A: Because that’s where the future buyers are

It’s really that simple. I probably sound like a broken record, but I still see vacant homes trying to sell for full market prices. And it’s just not working. Let me repeat: it’s just not working.

My old economics professor always said that the lottery was a tax for people who didn’t pay attention in math class. He meant that the odds of winning are so astronomical that buying a ticket is just a waste of money.

In a way, I feel the same about most vacant homes. Let’s look at the math:

Find the number of houses that sold in your region last year (let’s call this number “X”). Now compare X with what the home sales numbers were annually in the past 5 years. X is comparatively low. That is obviously not good news for home sellers. Unfortunately, home sales have trended downward (and are expected to continue to do so).

Now take X and cut it in half. What? Unfortunately, half of X is distressed home sales (foreclosure, REO, short sale, etc.). This “half of X” gives us the true number of people who are now shopping for your home (if it is listed for sale at close to full value). That’s not good.

So the math is basically saying that there are way fewer (way, way, way fewer!) home buyers out there for houses that are not distressed.

Note: For non-math majors (and lottery enthusiasts), you can also gather this information informally; just ask “How’s the sale process going?” to anyone who has their non-distressed home currently on the market for sale. They may respond with a half-laugh, menacing glance, or a choice word (not a nice one).

Then ask anyone who is trying to get a home loan the same question. You’ll probably get a similar response.

So many vacant homes are for sale. And many buyers can’t get a loan to buy your house. How could a win-win situation be created here?

This is why the rent-to-sell method of home selling is hot. Or, if you prefer to stick with the old song, rent-to-sell is “hot, hot, hot.”

How does rent-to-sell work? Buyers, who can’t qualify for a loan now, rent your home for 1-3 years until they qualify. Then they buy it at market price when the real estate market has rebounded. This solves the problem of home sellers eating the mortgage on a vacant home every month and buyers not having a place to call their own.

Rent-to-sell can be a great solution to escape the cold, expensive reality of a vacant home that isn’t selling!

Brett Furniss is the President & Owner of BDF Realty (“Charlotte’s Most Innovative Property Management & Investment Company”), and Rent-To-Sell Realty (“When You Need a New Solution to Sell Your Home”) which specialize in rent-to-own (lease options) and rent-to-sell homes. His newest book, A Real Estate Agent’s Complete Guide to Representing Rent-To-Own (Lease Option) Tenants (Delight Clients, Fill Vacant Homes, and Earn $2,250* Upfront! (*Minimum!)

Learn MoreCharlotte Property Management Weekly: #1 Way to Fill Rental Homes Quickly

As homes for sale sit and rentals continue to gain prominence in the residential real estate market across the country, concerned owners are wondering how to best fill their rental properties quickly. So are property managers.

“Everyday my house is empty costs me money! Besides the mortgage payment, it’s the other things that are absolutely killing me- utilities with this unusually cold and snowy winter, HOA dues rising, you name it. I need someone renting (or buying) my home!” is a common lament from homeowners with a vacant home on the market.

As a real estate investor and property manager in Charlotte, I feel your pain. I don’t like vacancies anymore than you. But there is a simple way to make your home attractive. And it addresses the most heard complaint, by far, that I hear about houses and why prospective tenants pass on them. And just what is this revelatory nugget?

Cleanliness. That’s it. Houses are typically not clean. Actually, it’s not that they are not clean technically. It’s that they are not clean enough. Prospective tenants want to see sparkle. They want to see their unblemished reflections coming off of stainless steel. They want to be able to eat off the floors. They want to lap cool spring water out of the toilets (well, I may be pushing it now…). The point is that they really like the houses to be much cleaner than they would normally keep them.

Recently, we switched to a different cleaning service that was more expensive. I would never think of adding expenses to our owner clients (especially in this economy), but I felt that our homes were not standing out as the rental market continued to get more and more crowded.

And it worked. I noticed our rate of conversions of visits to completed applications went up dramatically. This has gone on for months. Thorough, deep-cleaning was more effective than lowering the rental price. This has been especially effective for our rent-to-sell program where people want to fall in love with the house they are potentially buying.

I would challenge you to give it a try. When a house has been on the market for a while and has been getting visits (but no completed applications), resist the urge to lower the price and just pay the dollars to give the rental home a thorough scrubbing (or do it yourself, though I recommend professionals). See if it works!

Cleanliness is next to godliness, the saying goes. Reap the benefits of a shorter courting period with prospective tenants!

Brett Furniss is the President & Owner of BDF Realty (“Charlotte’s Most Innovative Property Management & Investment Company”), and Rent-To-Sell Realty (“When You Need a New Solution to Sell Your Home”) which specialize in rent-to-own (lease options) and rent-to-sell homes. His newest book, A Real Estate Agent’s Complete Guide to Representing Rent-To-Own (Lease Option) Tenants (Delight Clients, Fill Vacant Homes, and Earn $2,250* Upfront! (*Minimum!)

Learn MoreCharlotte Property Management Weekly: Mr. Smith’s Appointment Implies Real Estate’s Future is in Rent-To-Own & Rent-To-Sell

“Since they collapsed into conservatorship in September 2008, Fannie and Freddie have received $151 billion in taxpayer assistance. More will certainly be needed.”

“If this Mr. Smith goes to Washington as head of FHFA (Federal Housing Finance Agency), he will face a monumental challenge at a crucial time: how to protect taxpayers from even greater losses incurred by Fannie and Freddie.”

(Gretchen Morgenson in this week’s NY Times)

So, it looks like NC’s own Joseph Smith, Jr. will be tapped to run the FHFA. Big deal! Somebody’s got to do it, right? And when you’re looking for employment, the government seems to be the only people hiring, so it’s a logical step for him.

Who is this guy? I really have no idea. He’s been in the papers recently due to this appointment; all of the articles about him say that he has a reputation as “friend and rugged defender of the taxpayer.” I pay taxes so that sounds okay to me.

He is taking over an agency that is losing roughly $6B A MONTH over the past 27 months! Obviously, this agency has to be part of the government because after the first $18B loss quarter (or $72B loss year), it would be tough to keep his job in the private sector.

Anyway, what does his appointment mean? Let’s play his first day on the job out.

The first thing Mr. Smith does on his first day of work is ask his new secretary where the bathroom is and how many vacation days he has a year (everyone knows you can’t ask this in the interview!). The second thing he does is call his top guys and ask them how the heck they are losing so much taxpayer money. Their answers probably can be succinctly summarized into one statement, “We guaranteed a lot of bad loans to people who were not qualified enough to have them.”

Mr. Smith rubs his chin and says, “So, going forward, we should probably start only guaranteeing loans to more qualified people, right?” As his top lieutenants vigorously nod ascent and genuflect, he dismisses them from the room. “Sorry fellas, gotta go. It’s time for me to take it street-side and hug some oppressed taxpayers.”

His lieutenants quickly gather and surmise that “more qualified” probably means that Mr. Smith is saying FHFA needs to require “higher credit scores and down payments for loan applicants.” They pat themselves on the back for this revelation and scan the Washington Post to see what new DC restaurants would be good for lunch.

Back on Main Street, “more qualified” means a lot more people won’t be able to get loans to buy homes. It also means that a lot more people won’t be able to sell their homes (it takes two to tango, right?). And, furthermore, it means that real estate agents need to get used to doing even less brokerage business.

So all real estate agents need to pick up their equipment and go home? Hardly! Consumers still need to be able to transact real estate; the last time I checked, people are still marrying, divorcing, transferring, investing, having kids, sending kids into the real world, etc. They need to be able to acquire and dispose of homes.

The opportunity for real estate agents in the next few years will be placing potential buyers (who can’t get a loan now) into homes they will buy when they qualify for one; this means setting up rent-to-own (aka lease option or lease purchase) transactions. On the same token, it means opening up listings of vacant homes to rent-to-own tenants (also known as “rent-to-sell”).

Mr. Smith will be doing everything he can to stem massive loan losses. He is implicitly communicating to the real estate community that rent-to-own and rent-to-sell transactions will be the way to help customers achieve their goals over the next few years.

Will you change your business accordingly?

Brett Furniss is the President & Owner of BDF Realty (“Charlotte’s Most Innovative Property Management & Investment Company”), and Rent-To-Sell Realty (“When You Need a New Solution to Sell Your Home”) which specialize in rent-to-own (lease options) and rent-to-sell homes. His newest book, A Real Estate Agent’s Complete Guide to Representing Rent-To-Own (Lease Option) Tenants (Delight Clients, Fill Vacant Homes, and Earn $2,250* Upfront! (*Minimum!)

Learn MoreCharlotte Property Management Weekly: Rent-To-Own- Just like Burger King for Buyers and Sellers

A lot of banks don’t like Burger King. Why do I say that? It’s simply because they don’t want you to “Have it Your Way.”

Learn MoreCharlotte Property Management Weekly: The Top 3 Reasons Why Good Property Managers Matter More Now (Reason #3)

3. The skills needed for selling a home have (and will continue) to trend to more of a solution-based, “cash now, sell later” approach; outright sales are becoming scarcer as there are less qualified buyers available in the market

Learn More