Rising Costs of Hershey Bars & Rental Homes: Is Your Lease Keeping Up?

I was in the Harris Teeter grocery store the other day and was waiting in line at the register. As I perused some magazine covers (Prince Henry is doing what??), my eyes wandered over to the candy bars ($3.99 for a king-size Hershey bar??). That price point stuck in my mind. Weren’t these things $1.50 – $2.00 a few years ago??

The first inclination I typically have when I’m personally shocked at the expense of something for sale is to point the finger at myself. “You’re getting old, my old boy. Hard candy doesn’t cost a nickel anymore and the days of .99 gas (while getting it pumped by someone else in NJ!) are long gone. Calm down, son… In the modern world, things just cost more. Relax.”

Once I was able to get my emotions in check, I Googled the question and was met with an AI response: “Candy bars are more expensive due to a surge in cocoa prices, driven by supply shortages from poor harvests and diseases in West Africa. This has led major manufacturers like Hershey to raise prices or reduce package sizes to reflect the high cost of the primary ingredient.”

Hmmm… Makes logical sense. Recent cocoa price surges due to issues in West Africa is the answer to my candy bar conundrum. This is why the Hershey king-size candy bars cost 50-75% more in Charlotte now than five years ago! Maybe… So if that logic holds, then things calming down in West Africa will make my Hershey’s bar go back to costing 2 bucks at some point?

I think the answers provided for some price increases are tough to comprehend or believe. Whether we buy the reasons or not, the price increases themselves are very real nonetheless. And experience shows that the prices rarely come down after the crises pass. Businesses and consumers typically just need to adjust to paying more.

This factors into rental homes.

As a Charlotte property manager, I remember meeting with a new owner client a decade or so ago and the topic of what to charge for rent came up:

Me: It’s a nice- looking home! I think we could get the top of the market price for it- probably around $1,350.00/month. Would that work?

Client: Well, I’d prefer not to charge that much. I own the house and my costs are relatively low. I think with taxes, insurance, and the HOA fee my all-in costs are $500.00/month (oh, the good old days of low costs…). And when repairs come up, I’d like to have some extra rent to cover them. I’d prefer to keep the monthly rent under $1K to keep it affordable for the tenant.

Me: Wow- sure!

I don’t hear anything like that much anymore. It’s tougher to find margin between the actual costs of owning a rental home and the rent. All the cost components of rental home ownership have shot up: mortgage (home values & interest rates), taxes, home insurance, HOA fees, & repairs. “Things just cost more” is the simple real estate explanation for Hershey’s “runaway cocoa prices”.

With higher monthly costs, leases need to keep up with market-rate rent increases to avoid consistent losses. This doesn’t even factor in inevitable, higher costs for a new HVAC or roof which (since COVID) usually cost upward of $8K for smaller homes. Unfortunately, these cost increases are probably not going away. This means that even leases with great, long-term tenants need to be scrutinized if they are kept at an artificially low rate.

Much like Hershey passing on their cost increases to consumers (to my chagrin!), landlords need to factor in their increased costs when setting their rental pricing. Smart landlords will keep close tabs on market rental rates and make adjustments at periods of vacancy or lease renewal.

Happy Landlording!

Learn More

The “One Mistake” Case Against Rental Home Self-Management

“You don’t know what you don’t know.”

Socrates

It has been a life-long learning process for appreciating professionals in my adult life. Most of the time, this teaching did not come easily to me.

From fixing cars and watching them break down at inopportune times. Feeling physically poorly for months until I went to a doctor who had me better in days. Using bug spray to get rid of termites only to see them come back with a hungry vengeance until a proper exterminator was employed.

To be fair, fixing things on my own outside of my sweet spots isn’t always a losing effort. I’m always proud of myself when I can pull off some repair successfully in my house or submit some legal paperwork without any help. Go me!

Likewise, in property management, there is some definite positive reinforcement for self-managing:

“The last tenant I placed paid on time and left my rental home spotless!”

“No one is going to love my property like I do.”

“I do a lot of the repairs myself and save money.”

“Property managers are expensive!”

“The house is right by my house.” (writer’s note: that’s a double-edged sword…)

It is estimated that around 50% of all rental properties are self-managed, so it is prevalent. But despite the “tenant domination” stories told by some landlords at parties, it is not all roses. There really are midnight calls for stopped up toilets, tenants not paying rent that need to be evicted, and disgusting houses dropped into a landlord’s lap when a tenant leaves in the middle of the night. There is actual effort and stress in managing rental properties; to do it well requires time, sweat, and educational investment. No one can say it isn’t doable, though.

The biggest driver for self-management is saving money. I get that! There is a certain joy when all the money generated from the rental home goes directly into the bank account without any property management fee deductions. Months (or years) that this happily goes on is certainly a case for self-management; it probably comes to a few thousand dollars in potential savings per rental house a year.

But where things sometimes go awry in this calculation is that there is the “One Mistake”; this one miscalculation erases all accrued property management savings. Whether it is a legal one where a security deposit dispensation is not sent out in 30 days and the tenant who destroyed the house has the legal right to get it all back. Or when needed (or, sometimes it turns out, unneeded) repairs are made and the time and monetary investment keep ballooning due to unfamiliarity. Or a trusted vendor was employed who actually shouldn’t have been trusted. Or a tenant court date that keeps being pushed farther out due to not sending out proper notices while, concurrently, no rent is being paid.

The one-offs of learning the property management business can erase all the realized monetary savings and just leave uncompensated time that could have been better spent. That can be frustrating! And that’s the tough case against self-management.

The problem with avoiding the costly “One Mistake” is that it could happen in so many different areas. And sometimes things turn into “Two Mistakes” or more…

Property managers aren’t full-proof, but experience does offer some benefit for steering clear of these costly errors.

Happy Landlording!

Learn More

McAlister’s Deli “Service Fee” Strategy: Applicable to Rental Homes?

The (FTC) complaint alleges that (a large property management company) advertised monthly rental rates that failed to include mandatory junk fees that could total more than $1,700 yearly… These undisclosed fees ranged from “services” such as “smart home” technology and “utility management,” to air filter delivery and internet packages. Renters could not opt out of paying these fees.

(www.FTC.gov)

Some friends and I meet for a Bible study on Monday nights at the local McAlister’s Deli. After buying my sandwich one night, I started to peruse my receipt after paying. I was trying to figure out why my regular sandwich cost so much and looked at the bottom of the receipt. I saw the tax amount (can’t dodge that!), but above it was an itemized “Service Fee”. And here I thought I had just picked the sandwich up at the counter…

I clicked on an icon next to the aforementioned “Service Fee” and it offered a fuller explanation. “This fee is used to help pay for the restaurant’s app and website.” Surely, companies can’t charge for that as a mandatory fee.

Wait- or can they?

I always thought companies were only allowed to upcharge under the condition that they added more value. If McAlister’s allowed me to add another slice of cheese to my sandwich, I’m fine with them charging me more. If I wanted a bigger drink than what is in their value meal, I’d expect to pay more. But ordering on their app or website? Isn’t maintaining the on-line ordering portals the cost of doing business in today’s environment? And isn’t it cheaper and easier for them if I use them?

The line on chargeable value has gotten blurred in rental real estate as well. As property management companies have piqued Wall Street’s interest of late, maximizing revenue is being stressed and companies are getting really “creative”. Now I’m all for “revenue enhancement” as making more money is generally good. However, fees should be generated by providing tenants voluntary options that could make their lives easier or give them greater flexibility; mandatory fees for unwanted or unwarranted services could easily cross a line (see the FTC blurb above detailing the “value-added services” that incurred a $48M fine).

We are starting to have tenants ask us things like, “Is the rent really $1,800/month or are there hidden fees that are not mentioned?”. Being that these questions are being asked at all means this practice is becoming prevalent; legislation and more enforcement is probably on the horizon.

Landlords and property managers all aim to maximize revenue for their real estate investments and rightly so. However, we need to be cautious and make sure a fair value proposition is made. If any fees are questionable and wouldn’t withstand scrutiny, they should be scrapped. Landlords should be on notice and make sure general business practices on add-on fees stay on the right side of the law. “Service Fees” for common technology usage may only work in the food industry.

Happy Landlording!

Learn More

Bad Times to Buy Bank of America Stock and Charlotte Real Estate?

“(Warren) Buffett famously bought $5 billion worth of BofA’s (Bank of America’s) preferred stock and warrants in 2011 in the aftermath of the financial crisis, shoring up confidence in the embattled lender struggling with losses tied to subprime mortgages.”

7/30/24 CNBC.com article by Yun Li

“The Charlotte Regional Business Alliance reported about 113 people moved to the Charlotte metro every day between mid-2021 and mid-2022. That’s more than 41,000 people moving to the region every year.”

CLT Today 3/11/24

I remember hearing many years ago that the longer you live, the more economic cycles you’ll see. The “Dot.com Bubble” (2011) and COVID (2020) are ones I remember readily. But from a severity perspective, ‘The Great Recession” (2008-2010) was the most memorable and crushing.

Living in Charlotte, Bank of America casts a big shadow as it houses our largest corporate headquarters. And it got hammered during the Great Recession. Warren Buffett, arguably the greatest stock investor in history, invested $5B in 2011 when it was trading in the $5/share range. The lowest it had dipped to was $3.14 in 2009 and it was teetering along for years as it hemorrhaged losses from its Countrywide Financial acquisition.

At the time of his investment, Buffet said,

“Bank of America is a strong, well-led company, and I called Brian (Moynihan) to tell him I wanted to invest in it,” Mr. Buffett said in a statement. “I am impressed with the profit-generating abilities of this franchise, and that they are acting aggressively to put their challenges behind them. Bank of America is focused on their customers and on serving them well. That’s what customers want, and that’s the company’s strategy.”

Today, Bank of America’s stock price is around $40/share and Buffett has been in the news lately for selling some of his shares for billions in profit.

That’s what all investors want- buy low and sell high! But Buffett’s big payday took a long time to come to fruition as the stock languished for years. It was unknown when Bank of America, and the economy in general, would come back. But Buffett believed in Bank of America’s fundamentals.

We’re starting to see a real estate slowdown in the Charlotte market. There was a time, no too long ago, when a house on the market for sale would get multiple offers. Now, things have slowed, houses are sitting a bit longer, and price increases have waned.

Are home prices too costly? Interest rates too high? Economy too risky? A combination of these and other factors? Are these buyers right? Is it a good time to sit on the sidelines?

Or… is this price stabilization a great opportunity for real estate investors?

It’s tough to know for sure.

There are facts, though, that are undeniable. People continue to move to Charlotte every day in droves and have been for years. Everyone moving here needs a place to live. Housing is a needed commodity.

As Buffet said about his investment in Bank of America during an uncertain time, he wanted to get involved based on the company and its direction. Charlotte has an average of 113 people moving here everyday in need of housing.

Is this a bad time to buy Charlotte real estate? Or is it a great time?

Happy Landlording!

Learn More

Building God’s Temple & Lease Extensions: Are You Ready?

“King David rose to his feet and said: “Listen to me, my fellow Israelites, my people. I had it in my heart to build a house as a place of rest for the ark of the covenant of the Lord, for the footstool of our God, and I made plans to build it. 3 But God said to me, ‘You are not to build a house for my Name, because you are a warrior and have shed blood.’”

(1 Chronicles 28:2-3)

“If you fail to plan, you are planning to fail.”

Benjamin Franklin

King David loved God; they were tight. Towards the end of his life, he wanted to do something grand for God- so grand that he aspired to build the greatest temple in the world for Him! David shared this with Nathan, his resident spiritual advisor, and asked him to see if God would approve. Nathan inquired and relayed that God was not amenable to King David doing it; however, He told him that Solomon, his son and future successor, could build it.

King David did not use this as an excuse to sit on his hands. He asked God exactly what He wanted and proceeded to write down specific plans for Solomon to use. He not only detailed plans to build the temple and the surrounding buildings themselves, but for the all the items that would be kept in the temple. He mapped everything out precisely, even the weights of the lamps and tables and how the priests who would work there would contribute. All Solomon would need to do is dust off the plans and enact them when he was coronated. He would be ready to go!

For smart landlords, this is how lease extensions should be approached. When leases are expiring in the near future or tenants are proactively in contact about extending their leases, landlords should not be scrambling! A well-thought-out plan should be in place ready to be enacted.

As a Charlotte property manager, retaining good tenants is paramount. If we don’t hear from tenants prior to 80 days before their leases’ expiration, we start the “Lease Extension Plan”. This begins by running the nearby comparables to determine market price, checking their payment ledger to ascertain tenant quality, and making a recommendation to the owner on what we feel the lease extension price and terms should be.

Once we have finalized our lease extension offer, we e-mail it to the tenants somewhere between 60-75 days prior to lease expiration. This gives them plenty of time to ask any questions and make a decision. We also incentivize tenants to commit earlier as the proposed rental price is offered in tiers based on when they let us know their plans (example: “Let us know by 6/15, and the price will be $1,500.00/month… or if after 6/15, the price will be $1,600.00/month.”). We also offer options for month-to-month lease extensions (at a 10-20% premium to the existing rent based on current market conditions) and multi-year extensions (incentivized by allowing the rent to stay the same over the life of a longer lease term).

Other important factors we incorporate in the “Lease Extension Plan”:

- The new lease is written on the latest version to make sure that the owner has the best legal protection incorporating any recent changes to landlord law

- The tenant information is updated: Did anyone leave or is now joining the household? Did anyone get married/divorced? Name change(s)? New children? New pets to be accounted for?

- Are there any issues that we want to address with the tenant (or vice-versa) before we reup with them for another year or more?

Though King David was disappointed he would not be the one to build the temple, he made sure approved plans were prepared and ready when Solomon got the green light. Smart landlords will follow his example! With increased repair costs on rental home turnovers, keeping tenants by signing lease extensions is becoming more and more important to achieve rental home ROI.

Happy Landlording!

Learn More

Crushed by Cumulativeness: Rent Increases and Why the NFL Player Didn’t Sign Your Kid’s Football

“What a jerk! All he has to do is just sign his stupid name to ONE football and it would mean the world to Little Johnny. But instead he needs to hurry to the locker room to recount his millions of dollars!”

(Reaction of many parents after their child’s autograph request is snubbed)

I was talking to a local college football player (a kicker, if you must know) about what he was doing after he graduated in May. He said he was starting to figure that out being that he finally had some time to think about it.

Some time? He’s in college! I was thinking of how wasting time was sort of what my friends and I did during our undergraduate tenures…

“You don’t have any time? How did you get so scheduled out?”

He pulled out his team-issued iPad. “Do you see this? I had to look at this every day for the last five years; it told me where I was supposed to be and what I was supposed to be doing every hour of every day… Now, honestly, I’m adjusting to doing life without it.”

Wow! That sounds pretty demanding for a college kicker at a small-time football school. If I were him, I think I would have opted for intramural soccer.

Now let’s think about NFL players. There are even more football activities than college. They are travelling for training camp and games. If they don’t do well, they can be cut at any time. If they want to get better, they need to take the time to practice, lift weights, and study the playbook and game tape on their own. Then they have family, faith, friends, financial, and other real-life commitments- and everyone likes them and wants to be near them because they are wealthy and famous. They are super busy!

And then there are constant, on-going demands for their time. Want to be on a weekly talk show (aka NY Jets quarterback, Aaron Rodgers)? Make sure you cut an hour or two of every week for that. Endorsements? Autograph shows? Dinner with your wife? Your kid’s basketball games? Team functions? Mailing back football cards kids send them to sign? Your college wanting you to come back to accept an award on an off-week during the season?

If it was signing one football, that would be one thing. But it is signing one football in addition to an overpacked schedule.

So how does football player busyness fit into rent increases in today’s world?

A landlord may be heard muttering, “If a tenant can’t come up with an extra 5-10% for rent every year, maybe they shouldn’t be in the property in the first place!”

If it was just $100.00/month extra for rent every year, that would be one thing. But rental increases are not happening in a vacuum. Tenants have been absorbing increased rents in addition to increased costs for almost everything else they consume. Food, gas, car prices, car insurance, plane fares, restaurants, NFL tickets (another 4% increase in ticket prices was just announced by the worst team in the league, Carolina Panthers), etc.. Netflix just went up by another $2.00/month, for goodness sakes! Like small papercuts that keep happening, the bloodletting becomes very real eventually.

Cumulativeness can be crushing!

Property managers and smart landlords need to balance potential rental increases with killing the golden goose. Good tenants are an asset that maintain the property and pay down the underlying debt. Dumping another increased expense on them can be detrimental to both parties, especially if the tenant moves and the property needs to be repaired and put on the market again.

Good news! The college and NFL players don’t hate your kid. If they had an iPad with lots of empty time slots and/or few other commitments, I’m sure they would happily sign footballs most every time! And if rental increases are measured, good tenants will be able to absorb them and continue to be a reliable monthly partner.

Happy Landlording!

Learn More

Take it From NFL Quarterbacks: Be Thankful for Your Vendors

“…the Chiefs quarterback opted to go big with his show of appreciation for his offensive line with this year’s presents. Mahomes hooked up his protectors with sets of TaylorMade golf clubs, complete with custom bags featuring their jersey numbers and a box of balls for good measure.”

(Nick Selbe in Sports Illustrated: 12/21/22)

“Hi, I’m Dan Marino, and if anyone knows the value of protection, it’s me. So I take care of the hands that take care of me with Isotoner gloves.”

(Ace Ventura 1994)

“Rejoice always, pray without ceasing, in everything give thanks; for this is the will of God in Christ Jesus for you.”

(1 Thessalonians 5:16-18)

Every year I see articles talking about what Christmas presents NFL quarterbacks give to the members of their offensive line (typically around 10 guys). Looking at past gifts from the quarterbacks below, they seem to be pretty nice items and run the gamut:

Mac Jones (New England Patriots): Bitcoin

Carson Wentz (Indianapolis Colts): Bourbon, some meats, & Yeti coolers

Jalen Hurts (Philadelphia Eagles): Louis Vuitton travel bags

Dak Prescott (Dallas Cowboys): Air Jordan 11 Retro sneakers

These are not cheap gifts. When your livelihood (and long-term health!) depends on these offensive lineman preventing defenders from taking your head off, it is imperative to make sure they know they are appreciated. And now all the starting quarterbacks in the league make it a point to give nice gifts to the guys that try to keep them upright every game.

On that vein, I was listening to a video the other day and the instructor was talking about running a property management company. He reasoned that the main component of success was the ability to retain tenants; then he began his discourse into specific reasons why tenants did not re-sign their leases. The #1 reason, by far, was that repairs were not completed in a timely fashion. He argued that fixing things promptly is the silver bullet to keep tenants. Landlords can try other things like offering gift cards or flat screen TV’s as lease re-sign bonuses, but they offer little benefit if a tenant’s heating system hadn’t been functioning for 3 weeks the previous winter (like a now ex-neighbor told me recently had happened to him). To his point, most dissatisfied tenant’s Google reviews against property managers stem from delayed repair resolutions.

How does a landlord avoid lingering repair issues? First of all, work orders must get off the landlord’s desk and be directed to the appropriate vendors ASAP. Then, it’s all about vendor quality that will drive tenant satisfaction and property management success.

So, the lesson is… hire great vendors! Hire vendors who care. Hire vendors that realize that having the heat go down on a Friday afternoon means that it is going to be an awful weekend for the tenant if the work order is pushed until Monday. I’m amazed (and thankful!) that many of our vendors voice disappointment when they can’t get there the same day or a repair they made didn’t hold. They have empathy that it could be their families who are shivering at night or have no working plumbing. It takes a servant’s heart to put someone else’s family before your own.

Once a landlord finds these core, caring vendors and puts them to work, it is time to play the role of the thankful NFL quarterback. I’m not sure that necessarily means Louis Vuitton travel bags or TaylorMade golf club gifts (maybe some Isotoner gloves?), but I’d recommend the following four things we try to give our vendors:

- Loyalty: We give most of our business to our best vendors and keep it there

- Payment: We make sure invoices are paid consistently, in full, and when expected. They should be able to worry about their jobs, not exerting energy to collect due funds from us.

- Grace: Everyone messes up from time to time. Taking off people’s heads for honest mistakes isn’t going to help anyone. And when you do this long enough, you know that grace is a two-way street.

- Thankfulness: Let them know how much you appreciate their effort on a day-to-day basis. We all like to feel like what we do is noticed positively.

NFL quarterbacks may have millions of dollars to shower their guys with Bitcoin “thank you” gifts, but sometimes the smaller gestures above can go even further. Give thanks and take care of the hands that take care of you!

Have a wonderful Thanksgiving & Happy Landlording!

Learn More

“100% Guarantee For Your Rental Home!” Delightful or Sour?

Tommy: Here’s how I see it. A guy puts a guarantee on the box ’cause he wants you to feel all warm and toasty inside.

Ted: Yeah, makes a man feel good.

Tommy: ‘Course it does. Ya think if you leave that box under your pillow at night, the Guarantee Fairy might come by and leave a quarter.

Ted: What’s your point?

Tommy Boy (1995)

My 9-year old son was eating frozen blueberries a few weeks ago and started to complain about them. “They’re so sour! Gross!”

I advised him, “Well, that’s too bad. You get some good ones, and you get some bad ones. It’s the way life goes…” Then I patted myself on the back for imparting some timeless, Forest Gump parenting advice.

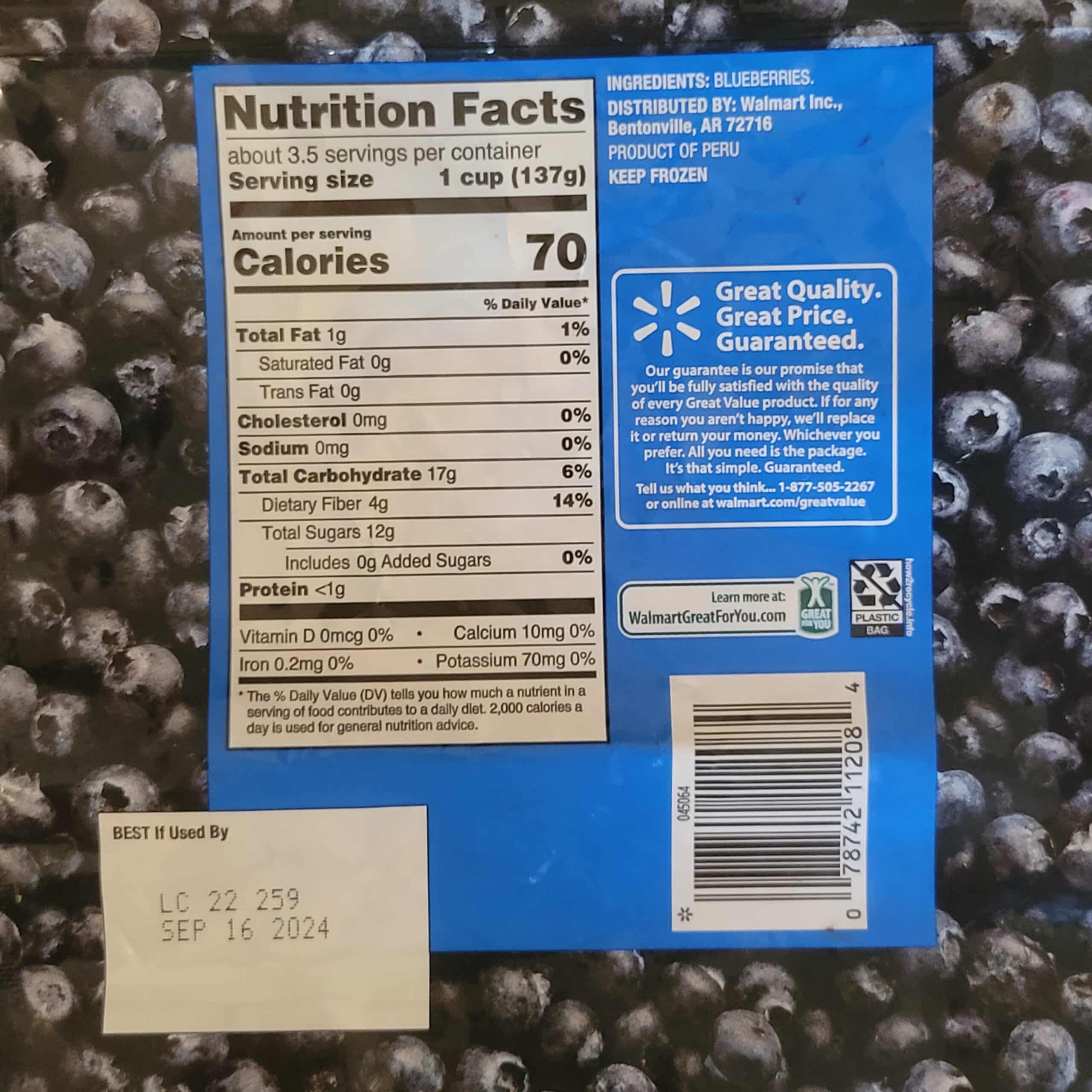

Sometime later, he complained again- and then three or four other times after eating these blueberries. Finally, I grabbed the package off the table and saw it was the “Great Value” Wal-Mart brand. My eyes narrowed on the “Great Quality. Great Price. Guaranteed.” guarantee printed on the back. Verbatim, it read:

If for any reason you aren’t happy, we’ll replace it or return your money. Whichever you prefer. All of you need is the package. It’s that simple. Guaranteed.

Now was the time to teach my son about the advantage of paying attention and reading the fine print! “Son, we’re going to Wal-Mart and you’re going to take care of it.” “Dad, are you sure we can bring this package in and they’ll give us the money back? I’ve already eaten half of them…” “Yes, son. It’s that simple. Guaranteed!”

After my son negotiated that he could keep the $2.99 windfall and put it towards a pack of football cards, he signed on to this gambit. We drove over to Wal-Mart and, from a distance, I watched my son explain to the customer service person that the blueberries were sour and that he wanted a refund. After a minute or so, he walked away from the counter, defeated, and let me know that we could swap it out for another bag of (sour) blueberries; there was no option of getting football card money instead.

Now Dad was sure there was a misunderstanding! It’s guaranteed! It’s simple! And it’s a $2.99 charge to a multi-billion dollar conglomerate! Well, yours truly fared no better when I approached the customer service desk and was promptly (but nicely) shut down. If I didn’t have the receipt or credit card it was bought with, their hands were tied. There was nothing that could be done.

Undeterred, as my young kids trolled the Wal-Mart aisles unattended, I called the #800 number that was located under the guarantee. After a 14-minute phone call of providing serial numbers, date of purchase, and personal information, the customer service representative (who was also very nice) said that we would receive a $5.00 Wal-Mart gift card mailed to us within 2 weeks, but no cash. When we got home, I sent a message through the “Great Value Guarantee” website and they referred me to the in-store customer service desk for any refund requests. I wrote back saying that was where it all started! Then I never heard back. Ugh!

If for any reason you aren’t happy, we’ll replace it or return your money. Whichever you prefer. All of you need is the package. It’s that simple. Guaranteed.

The final scorecard read: (1) in-store visit, (1) 14-minute phone call, (1) web inquiry, & (1) 2-week wait for a $5.00 store credit. So, obviously, it’s not that simple. And it’s far from guaranteed. And we are talking about getting $2.99 back from Wal-Mart which they explicitly stated was a sure thing on the package itself.

Great story! But what’s your point? What does getting a cash refund for a sour bag of Great Value frozen blueberries have to do with property management?

A lot, actually. It’s about the danger of relying on corporate guarantees when picking vendors, especially in real estate. Whether it is for home warranty insurance against bigger ticket items breaking down (HVAC systems, roofing, appliances, etc.), costly property management occurrences (eviction, pet issues, etc.), or just getting money back from poor work (a flooring vendor recently), it is difficult to get companies to honor them. No company wants to pay (not even $2.99!) and there is always a reason why the guarantee doesn’t apply. It’s frustrating, (super) time-consuming, and borderline unethical at times.

But that doesn’t stop them from being ubiquitous:

- Home warranty companies: “If your HVAC system goes down and it can’t be fixed, we’ll buy you a new one! It’s so simple. Guaranteed!”

- Property management companies: “If there is an eviction or pet damage, we’ll cover the costs- It’s so simple! Guaranteed!”

- Wal-Mart: “If for any reason you aren’t happy, we’ll replace it or return your money. Whichever you prefer. All of you need is the package. It’s that simple. Guaranteed.”

Life is too short. The best bet is to pick a company that consistently offers quality blueberries instead of trying to be compensated on the backend when they are sour. Getting the $2.99 back is arduous at best, and unfortunately, usually fruitless. Be wary of upfront guarantees and concentrate more on established track records of excellence!

Happy Landlording!

Learn More

Don’t Be a Desperate Housewife (or Landlord), Just Push the Right Buttons

“Desperate times call for desperate measures.”

Hippocrates

Typing the word “desperate” makes me think of the old TV show, Desperate Housewives. The story centered on four suburban women who were neighbors. They found themselves making risky choices in order to look good, be fulfilled, and live the lives they thought would make them happiest. This made their lives hectic and drama-filled. And it also made it one of the most successful shows on TV for its 8-year run.

However, no one really wants to live the way they did; it may be entertaining to watch, but it’s not peaceful. Desperate is not desirable.

Desperation can elicit hopelessness and cause knee-jerk reactions:

I never think anyone is going to marry me! So I’ll lower my standards and date anyone and try to make it fit.

I don’t have any money and lots of debt. I’ll rob a bank.

We need to win a championship this year or the fan base will be calling for my head. I’ll trade away future draft picks, get a marginally better player now, and hope it works out.

We see it in all walks of life in many different situations. Desperate situations make people feel that they have little choice but to make hasty and risky decisions. And these decisions generate results that usually share one common trait- they are poor.

For landlords, they typically begin to feel desperate when their rental properties are vacant and they need tenants to move-in and start paying rent. Things look bleak as time rolls by and there has been:

- Financial bleeding: mortgage payment, management costs, utilities, lawn mowing

- Vandalism and/or squatting while vacant

- Only substandard applicants applying

It’s tough. There is pressure on landlords to accept the first person that has the deposit and first month’s rent to put down. “Just move in quickly, please!! We need this off the market to get the rent coming in!”

As a Charlotte property manager, we are not immune to this either. We get some version of this at times:

Aren’t you the professional?? Why is my property empty? What does your marketing look like? It doesn’t seem to be working, bud!! I could do better than this myself!

Desperation can take hold… And it takes discipline to stick to the fundamentals and not succumb to the pressure.

When a property has sat on the market for longer than expected, the key is not to panic! Slow down, take a breath, and push the right buttons:

If there are no showings of the property:

- Double-check the marketing, add/replace pictures, make sure the home is coming up in on-line searches. Then see if any showings happen. If not, go to step #2.

- The price is too high. Lower it ASAP. Prospective applicants are not seeing the value on-line versus other homes.

If showings are being generated:

- Ask people who have seen it why they are not filling out an application. It will usually come down to some cosmetic issue. Take care of the issue! Note: Some “cosmetic issues” are personal preference- if it is not a major flaw and only one or two people comment on it, it might not make sense to address it if it is costly. If almost everyone mentions it, it either needs to be fixed or the price needs to be lowered (or both).

I remember we had a large house on the market that “desperately” needed work. We did not want to pay for it (it was going to cost a lot to get to market shape) and we were hoping we could slide by with one more rental cycle before ordering the major (cosmetic) fix-up. We went a few months with several showings, but no approvable renters from those who filled out an application. Most non-applicants who visited the home cited a few issues they wanted addressed. What to do?

The easiest way path is to give in to the desperation, roll the dice, and approve a risky tenant. In contrast, experienced landlords will reject substandard tenants, double-check the marketing, fix any reasonable home repair issues, and lower the price. It’s better to wish you had a tenant than wish you didn’t.

Don’t fall for the feeling of desperation and press the panic button! Stick to the fundamentals and your future self will thank you for dodging the money/time/emotional sinkhole of the eviction process. Don’t let yourself become another desperate resident of Wisteria Lane!

Happy Landlording!

Learn More

Real Estate Investing: Preparing for Recession

“Where there is no vision, the people perish…”

Proverbs 29:18

Well, we started with a Bible verse, so it’s a good time to go into the story of Joseph in the Bible (located in Genesis 41).

To paraphrase, Pharoah, the leader of Egypt, had two dreams that no one could interpret. His chief cupbearer (and a former jailbird) remembered that he knew a guy in the joint who had (successfully) interpreted dreams for him and his buddy a few years back. He told Pharoah about this Joseph guy and Pharoah had him sent for.

Joseph said God had revealed both of Pharoah’s dreams to him and they had the same message; Egypt and the surrounding lands would have seven years of incredible plenty followed by seven years of devastating famine. He advised, “Let the Pharoah look for a discerning and wise man and put him in charge of the land of Egypt. Let Pharoah appoint commissioners over the land to take a fifth (20%) of the harvest of Egypt during the seven years of abundance… This food should be held in reserve for the country, to be used during the seven years of famine that will come upon Egypt…”

He concurs and appoints Joseph to head this newly created post and things go as predicted. Egypt is the only place that has food when the years of famine come, and Joseph is administering it on Pharoah’s behalf. The Egyptians and the people of surrounding lands are forced to sell Pharoah all their possessions and land just to get food.

To bring this back into the realm of real estate investing, landlords are clearly in the time of plenty as property values and rental prices have been on a growth curve for the last ten years. To boot, interest rates have been historically low (and really still are) which allow for low borrowing costs and has made for a robust sales market. Many landlords have used this as a time to sell some of their “dog” properties, make improvements and raise the rents on their existing properties, buy some new ones, and refinance/eliminate debt.

Recently, interest rates have more than doubled and many economists (none with divine inspiration like Joseph to my knowledge…) claim a recession is around the corner. If that’s true, the housing market could take a sharp correction which could be a great opportunity for prepared investors.

I have vague recollections from the last housing correction from 2008-2012. I did not buy any investment properties then; I was too concentrated on keeping my existing rental homes afloat as rents were low during that time period. I remember that selling homes was really hard; buyers were scarce! Many sellers were just giving their houses back to the bank or using “short sales” as the banks would take a loss on part of the loan during the sale. I remember thinking, “What’s wrong with me? As a wanna-be real estate investor, how am I not buying homes now? These houses are going for a steal and they seem to be all over the place!”

The thing that was wrong was that I could not get a decent loan and did not have much cash on hand. So, I needed to sit on the sidelines like most other people until the economic waves grew more favorable. But the buyers who were prepared got some great deals!

The investment challenge now is to be more like Joseph and be prepared for any possible famine while things are favorable. If the right investment comes along during any upcoming recessionary period, I’d like to be able to snap it up (while simultaneously staying solvent during any prolonged economic slump). Preparation now can pay huge dividends later.

Happy Investing & Landlording!

Learn More